Community Reinvestment Act Notice

Under the federal Community Reinvestment Act (CRA), the Federal Deposit Insurance Corporation (FDIC) evaluates our record of helping to meet the credit needs of this community consistent with safe and sound operations. The FDIC also takes this record into account when deciding on certain applications submitted by us.

Your involvement is encouraged.

You are entitled to certain information about our operations and our performance under the CRA. You may review today the public section of our most recent CRA evaluation, prepared by the FDIC, and a list of services provided at this branch. You may also have access to the following additional information, which we will make available to you at this branch within five calendar days after you make a request to us: (1) a map showing the assessment area containing this branch, which is the area in which the FDIC evaluates our CRA performance in this community; (2) information about our branches in this assessment area; (3) a list of services we provide at those locations; (4) data on our lending performance in this assessment area; and (5) copies of all written comments received by us that specifically relate to our CRA performance in this assessment area, and any responses we have made to those comments. If we are operating under an approved strategic plan, you may also have access to a copy of the plan.

At least 30 days before the beginning of each quarter, the FDIC publishes a nationwide list of the banks that are scheduled for CRA examination in that quarter. This list is available from the Regional Director, FDIC, 1100 Walnut Street, Suite 2100, Kansas City, MO 64106. You may send written comments about our performance in helping to meet community credit needs to the President Kellen Shebeck, PO Box 247, Underwood, MN 56586 and the FDIC Regional Director. You may also submit comments electronically through the FDIC's Web site at www.fdic.gov/regulations/cra. Your letter, together with any response by us, will be considered by the Federal Deposit Insurance Corporation in evaluating our CRA performance and may be made public.

You may ask to look at any comments received by the FDIC Regional Director. You may also request from the FDIC Regional Director an announcement of our applications covered by the CRA filed with the FDIC. We are an affiliate of Underwood Bancshares, a bank holding company. You may request from the Officer in Charge of Supervision, Federal Reserve Bank of Minneapolis, 90 Hennepin Ave, Minneapolis, MN 55480-0291 an announcement of applications covered by the CRA filed by bank holding companies.

Public Disclosure

COMMUNITY REINVESTMENT ACT

PERFORMANCE EVALUATION

Farmers State Bank of Underwood

Certificate Number: 1017 4

110 Main Street

Underwood, Minnesota 56586

Federal Deposit Insurance Corporation

Division of Depositor and Consumer Protection

Kansas City Regional Office

1100 Walnut Street, Suite 2100

Kansas City, Missouri 64106

This document is an evaluation of this institution's record of meeting the credit needs of its entire community, including low- and moderate-income neighborhoods, consistent with safe and sound operation of the institution. Ibis evaluation is not, nor should it be construed as, an assessment of the financial condition of this institution. The rating assigned to this institution does not represent an analysis, conclusion, or opinion of the federal financial supervisory agency concerning the safety and soundness of this financial institution.

Institution Rating

INSTITUTION'S CRA RATING: This institution is rated Satisfactory.

An institution in this group has a satisfactory record of helping to meet the credit needs of its assessment area, including low- and moderate-income neighborhoods, in a manner consistent with its resources and capabilities.

The following points summarize the bank's Community Reinvestment Act (CRA) performance:

- The loan-to-deposit ratio is reasonable given the institution's size, financial condition, and assessment area credit needs.

- The institution made a substantial majority of its small business, small farm, and home mortgage loans in its assessment area.

- The geographic distribution of loans reflects reasonable dispersion throughout the assessment area.

- The distribution of borrowers reflects reasonable penetration among businesses and farms of different sizes and individuals of different income levels.

- The institution has not received any CRA-related complaints since the previous evaluation; therefore, this factor did not affect the rating.

Description of Institution

Farmers State Bank of Underwood is headquartered in Underwood, Minnesota. The institution is owned by Underwood Bancshares, Inc., a one-bank holding company also located in Underwood. In addition to its main office, the institution operates three branches in Dalton, Fergus Falls and Rothsay, Minnesota. The Fergus Falls branch, which is new since the prior evaluation, opened on July 1, 2020. The bank received a Satisfactory rating at its previous FDIC Performance Evaluation, dated February 3, 2020, based on Interagency Small Bank Examination Procedures.

Farmers State Bank of Underwood offers traditional loan products including home mortgage, commercial, consumer, and agricultural loans. The bank’s business focus continues to be divided amongst commercial, home mortgage, and agricultural lending. Farmers State Bank of Underwood also participates in government-sponsored loan programs through entities including the Small Business Administration (SBA) and the Farm Service Agency. Notably, the bank participated in the SBA-administered Paycheck Protection Program and originated 263 loans totaling $5,844,624 between April 2020 and May 2021. This program assisted small business and farm operators struggling with the impact of the COVID-19 pandemic. The bank also maintains referral arrangements to assist customers in obtaining home mortgage loans on the secondary market. Farmers State Bank of Underwood provides a line of standard deposit products as well, including checking and savings accounts and certificates of deposit. In addition to traditional banking services, the institution offers online and mobile banking, mobile check deposit, electronic bill payment, and electronic periodic statements.

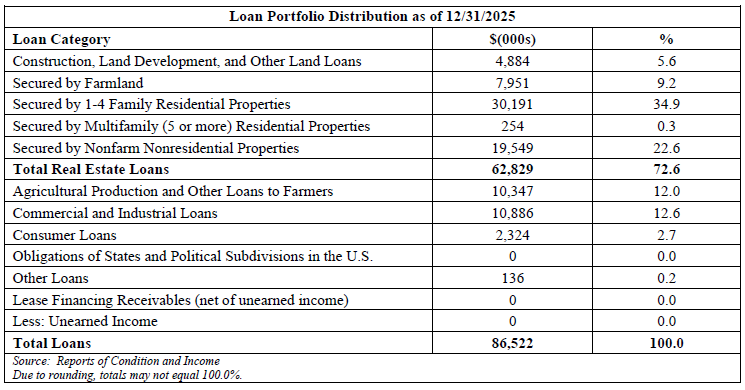

As of December 31, 2025, Farmers State Bank of Underwood reported total assets of $113,514,000; total loans of $86,522,000; and total deposits of $99,727,000. The following table illustrates the loan portfolio, which is primarily composed of commercial, residential real estate, agricultural lending. This is generally consistent with the previous evaluation. However, agricultural lending represents a slightly smaller portion of the loan portfolio by dollar volume compared to the previous evaluation. Examiners did not identify any financial, legal, or other impediments that would limit the institution’s ability to meet the credit needs of its assessment area.

Description of Assessment Area

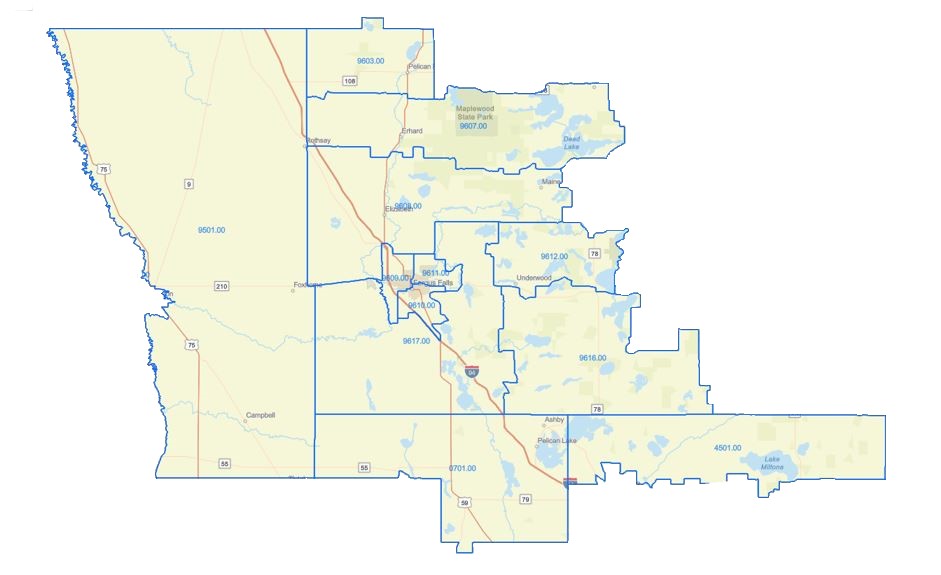

The CRA requires each financial institution to define one or more assessment areas within which its performance will be evaluated. Farmers State Bank of Underwood has designated a single continuous assessment area in west central Minnesota that consists of nonmetropolitan geographies. The assessment area is comprised of the northern portions of Douglas and Grant counties, the western half of Otter Tail County, and a majority of Wilkin County, with the exception of census tract 9502, which encompasses the City of Breckenridge, Minnesota.

According to the 2020 U.S. Census, the assessment area includes 1 moderate-, 10 middle-, and 1 upper-income census tracts. This reflects a change from the prior evaluation, at which time the assessment area was comprised of 10 middle- and 2 upper-income census tracts per 2015 American Community Survey (ACS) data. Specifically, census tract 9608 in Otter Tail County changed from upper- to middle-income following the 2020 Census, while census tract 9609 in Otter Tail County changed from middle- to moderate-income. The bank’s main office in Underwood and Rothsay branch are in middle-income tracts, while the Dalton branch is in an upper-income tract and the Fergus Falls branch is in the sole moderate-income tract.

Economic and Demographic Data

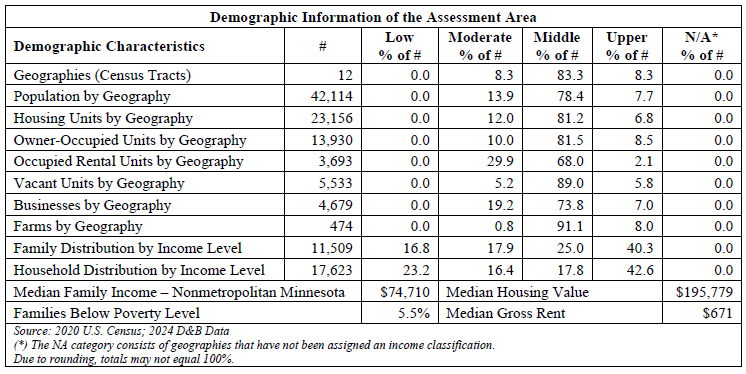

The following table illustrates select demographic characteristics of the assessment area.

The following table illustrates select demographic characteristics of the assessment area.

Particularly, Otter Tail, Douglas, and Grant counties contain a number of lakes, which makes it a popular resort and seasonal destination for water and land activities. Tourism and its ancillary services are the primary economic drivers within the assessment area. As presented above, there are 23,156 housing units in the assessment area. Of these, 60.2 percent are owner-occupied, 15.9 percent are occupied rental units, and 23.9 percent are considered vacant. As such, the vacancy rate in the assessment area is much higher than in traditional markets. This higher vacancy rate is attributed to the significant portion of the vacant units classified for seasonal, recreational, or occasional use due assessment area’s presence in the lakes community.

The Federal Financial Institutions Examination Council (FFIEC)-estimated median family income level is used to analyze home mortgage loans under the Borrower Profile criterion. The following table illustrates the FFIEC-estimated median family income ranges for nonmetropolitan Minnesota in 2025.

Competition

Farmers State Bank of Underwood operates in a moderately competitive market for financial services. According to June 30, 2025 FDIC Deposit Market Share data, there are 29 financial institutions operating 58 offices within Douglas, Grant, Otter Tail, and Wilkin counties. Of these institutions, Farmers State Bank of Underwood ranked 13th with a deposit market share of 2.4 percent. However, this data does not include deposit market share information for credit unions, which are also present in the assessment area.

Farmers State Bank of Underwood is not required to collect or report its small business, small farm, or home mortgage loan data and has elected not to do so. As such, the tables presented in the Lending Test do not include direct comparisons to aggregate lending data. However, the aggregate lending data provides an indication of the level of demand and competition for small business, small farm, and home mortgage loans. There is a significant level of demand and competition for small business loans in the assessment area, as evidenced by 2024 CRA aggregate CRA data, which is the most recent year available, shows that 55 lenders reported 1,823 small business loans originated or purchased within the assessment area. Similarly, 2024 aggregate CRA data shows that 23 lenders reported 538 small farm loans originated or purchased within the assessment area. These figures do not include the number of loans originated by smaller institutions that are not required to report lending data but operate within the assessment area. The overall volume of small business and small farm lending reflects a competitive market. Furthermore, there is an increased level of competition for home mortgage loans in the assessment area amongst banks, credit unions, and non-depository mortgage lenders, as evidenced by 2024 HMDA aggregate data, which is the most recent year available. In 2024, 138 lenders reported 983 home mortgage loans originated or purchased within the assessment area.

Community Contacts

As part of the evaluation process, examiners contact third parties active in the assessment area to assist in identifying the credit needs. This information helps determine what credit opportunities are available and whether local financial institutions are responsive to the area’s credit needs. For this evaluation, examiners reviewed an existing community contact interview conducted with a representative from an organization that provides funding and technical assistance to businesses in west central Minnesota.

The community contact indicated that the economy is currently stable; however, several factors have negatively impacted local communities, namely low workforce numbers, expensive moves to automation, patchy broadband infrastructure in rural areas, and limited openings for childcare. The contact added that there is a low quantity of adequate and affordable housing and that many of these properties may need a great deal of improvements to sell. Apartments are also limited, and new construction is even more rare. The contact commented on area businesses as well, noting that there have been few business closures due to COVID-19 relief money; however, with COVID-19 reserves diminishing, in addition to inflation, small businesses are beginning to struggle. Although the community contact did not directly say there is a lack of access to capital, higher interest rates and bank lending limits appear to be negatively impacting borrowers more frequently. Further, lenders appear to have become more conservative with loan-to-value ratios, especially with start-up businesses.

Credit Needs

Considering information from the community contact, bank management, and demographic and economic data, examiners determined commercial, agricultural, and home mortgage loans all represent credit needs within the assessment area.

Considering information from the community contact, bank management, and demographic and economic data, examiners determined commercial, agricultural, and home mortgage loans all represent credit needs within the assessment area.

Scope of Evaluation

General Information

This evaluation covers the period from the prior evaluation dated February 3, 2020, to the current evaluation dated February 2, 2026. Examiners used Interagency Small Bank Examination Procedures to evaluate Farmers State Bank of Underwood’s CRA performance. These procedures evaluate the institution’s performance according to the Lending Test criteria as detailed in the Appendices.

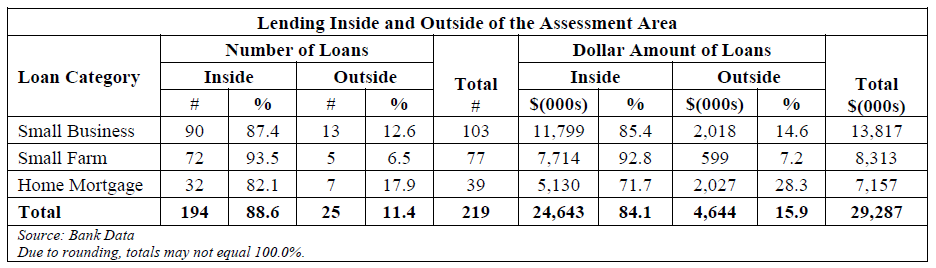

For the Assessment Area Concentration analysis, examiners reviewed all small business, small farm, and home mortgage loans that were originated in 2025. Loan data including extensions and renewals was not available. During this timeframe, Farmers State Bank of Underwood originated 103 small business loans totaling $13,817,000; 77 small farm loans totaling $8,313,000; and 39 home mortgage loans totaling $7,157,000. To analyze the Geographic Distribution criterion, all small business, small farm, and home mortgage loans located within the assessment area were reviewed. As revenue information was not readily available, examiners selected random samples of the small business and small farm loans that were located within the assessment areas for the Borrower Profile analysis. The samples included 41 small business loans and 36 small farm loans, totaling $5,320,000 and $3,435,000, respectively. Finally, all 32 home mortgage loans in the assessment area were reviewed for the Borrower Profile analysis, totaling $5,130,000.

D&B data for 2024, the most recent year available, provided a standard of comparison for small business and small farm loans. D&B is an entity that maintains a database of information on businesses and farms using a variety of resources including public records, trade references, and surveys. D&B data is used as a general indicator of the local economy and includes information from only those entities that voluntarily report. U.S. Census data from 2020 and FFIEC information from 2025 were used as a standard of comparison for home mortgage lending.

The bank’s record of originating small business and small farm loans contributed more weight to overall conclusions due to the larger loan volumes when compared to home mortgage lending throughout the review period. In addition, while both number and dollar volume of loans are presented, examiners emphasized performance by number of loans because the number of loans is a better indicator of the geographies, businesses, farms, and individuals served.

Home Mortgage Loans

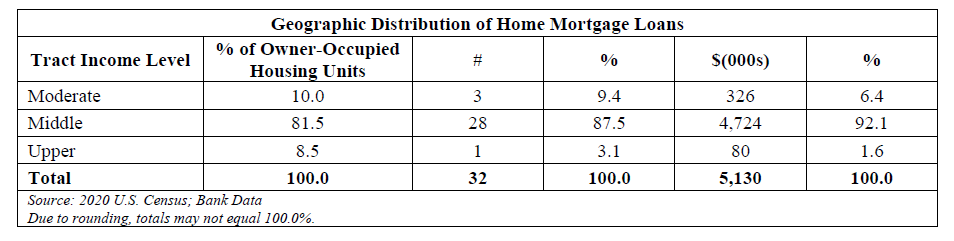

The geographic distribution of home mortgage loans reflects reasonable dispersion throughout the assessment area. As shown in the table below, the bank’s performance in the moderate-income tract is comparable to 2020 U.S. Census data.

Small Business Loans

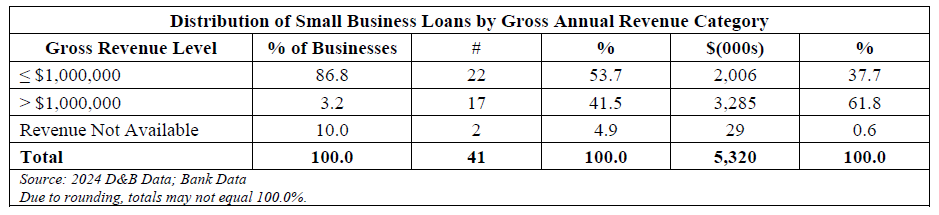

The distribution of borrowers reflects reasonable penetration to businesses of different revenue sizes. As shown in the table below, the bank’s lending performance to businesses with gross annual revenues of $1 million or less lags the comparable demographic data.

While Farmers State Bank of Underwood is not required to and does not report small business loans under CRA, aggregate CRA data provides context about the size of businesses to which other banks are lending. Aggregate data from 2022 through 2024 revealed that, on average, reporting banks made 58.9 percent of small business loans in the assessment area to businesses with gross annual revenues of $1 million or less. Therefore, the bank’s lending performance is comparable with the average aggregate data. Finally, the 41 sampled loans were made to 31 borrowers. Therefore, when considering the bank’s performance by borrowers, 21 borrowers or 67.7 percent had revenues less than or equal $1 million. Further, as previously mentioned, the bank participated in the SBA’s Paycheck Protection Program, in which the bank originated 263 loans totaling $5,844,624 between 2020 and 2021, demonstrating their willingness to support small businesses. Considering these factors, the bank’s performance is considered reasonable.

Finally, 21.9 percent of the home mortgage loans originated in 2025 are commercial purpose/non-owner occupied, such as rental properties, which result in a borrower income level of not available (NA). This skews the lending performance to all income levels. When considering these factors, the bank’s performance is reasonable.

American Community Survey (ACS): A nationwide United States Census survey that produces demographic, social, housing, and economic estimates in the form of five-year estimates based on population thresholds.

Area Median Income: The median family income for the MSA, if a person or geography is located in an MSA; or the statewide nonmetropolitan median family income, if a person or geography is located outside an MSA.

Assessment Area: A geographic area delineated by the bank under the requirements of the Community Reinvestment Act.

Census Tract: A small, relatively permanent statistical subdivision of a county or equivalent entity. The primary purpose of census tracts is to provide a stable set of geographic units for the presentation of statistical data. Census tracts generally have a population size between 1,200 and 8,000 people, with an optimum size of 4,000 people. Census tract boundaries generally follow visible and identifiable features, but they may follow nonvisible legal boundaries in some instances. State and county boundaries always are census tract boundaries.

Combined Statistical Area (CSA): A combination of several adjacent metropolitan statistical areas or micropolitan statistical areas or a mix of the two, which are linked by economic ties.

Consumer Loan(s): A loan(s) to one or more individuals for household, family, or other personal expenditures. A consumer loan does not include a home mortgage, small business, or small farm loan. This definition includes the following categories: motor vehicle loans, credit card loans, home equity loans, other secured consumer loans, and other unsecured consumer loans.

Core Based Statistical Area (CBSA): The county or counties or equivalent entities associated with at least one core (urbanized area or urban cluster) of at least 10,000 population, plus adjacent counties having a high degree of social and economic integration with the core as measured through commuting ties with the counties associated with the core. Metropolitan and Micropolitan Statistical Areas are the two categories of CBSAs.

Family: Includes a householder and one or more other persons living in the same household who are related to the householder by birth, marriage, or adoption. The number of family households always equals the number of families; however, a family household may also include non-relatives living with the family. Families are classified by type as either a married-couple family or other family. Other family is further classified into “male householder” (a family with a male householder and no wife present) or “female householder” (a family with a female householder and no husband present).

Full-Scope Review: A full-scope review is accomplished when examiners complete all applicable interagency examination procedures for an assessment area. Performance under applicable tests is analyzed considering performance context, quantitative factors (e.g., geographic distribution, borrower profile, and total number and dollar amount of investments), and qualitative factors (e.g., innovativeness, complexity, and responsiveness).

Geography: A census tract delineated by the United States Bureau of the Census in the most recent decennial census.

Home Mortgage Disclosure Act (HMDA): The statute that requires certain mortgage lenders that do business or have banking offices in a metropolitan statistical area to file annual summary reports of their mortgage lending activity. The reports include such data as the race, gender, and the income of applicants; the amount of loan requested; and the disposition of the application (approved, denied, and withdrawn).

Home Mortgage Loans: Includes closed-end mortgage loans or open-end line of credits as defined in the HMDA regulation that are not an excluded transaction per the HMDA regulation.

Housing Unit: Includes a house, an apartment, a mobile home, a group of rooms, or a single room that is occupied as separate living quarters.

Limited-Scope Review: A limited scope review is accomplished when examiners do not complete all applicable interagency examination procedures for an assessment area. Performance under applicable tests is often analyzed using only quantitative factors (e.g., geographic distribution, borrower profile, total number and dollar amount of investments, and branch distribution).

Low-Income: Individual income that is less than 50 percent of the area median income, or a median family income that is less than 50 percent in the case of a geography.

Market Share: The number of loans originated and purchased by the institution as a percentage of the aggregate number of loans originated and purchased by all reporting lenders in the metropolitan area/assessment area.

Median Income: The median income divides the income distribution into two equal parts, one having incomes above the median and other having incomes below the median.

Metropolitan Division (MD): A county or group of counties within a CBSA that contain(s) an urbanized area with a population of at least 2.5 million. A MD is one or more main/secondary counties representing an employment center or centers, plus adjacent counties associated with the main/secondary county or counties through commuting ties.

Activities Reviewed

As described earlier, Farmers State Bank of Underwood has a varied lending focus. This conclusion is based on the bank’s business strategy, lending activity during the evaluation period, and Reports of Condition and Income data. The December 31, 2025 Reports of Condition and Income revealed that commercial and residential real estate lending comprise the largest portions of the loan portfolio followed by agricultural lending. Therefore, examiners reviewed all three primary products during the evaluation. Bank records indicate that the lending focus and product mix remained generally consistent throughout the evaluation period. Therefore, examiners selected 2025, the most recent calendar year, as the review period. This time frame was considered representative of the bank’s performance during the entire evaluation period.

For the Assessment Area Concentration analysis, examiners reviewed all small business, small farm, and home mortgage loans that were originated in 2025. Loan data including extensions and renewals was not available. During this timeframe, Farmers State Bank of Underwood originated 103 small business loans totaling $13,817,000; 77 small farm loans totaling $8,313,000; and 39 home mortgage loans totaling $7,157,000. To analyze the Geographic Distribution criterion, all small business, small farm, and home mortgage loans located within the assessment area were reviewed. As revenue information was not readily available, examiners selected random samples of the small business and small farm loans that were located within the assessment areas for the Borrower Profile analysis. The samples included 41 small business loans and 36 small farm loans, totaling $5,320,000 and $3,435,000, respectively. Finally, all 32 home mortgage loans in the assessment area were reviewed for the Borrower Profile analysis, totaling $5,130,000.

D&B data for 2024, the most recent year available, provided a standard of comparison for small business and small farm loans. D&B is an entity that maintains a database of information on businesses and farms using a variety of resources including public records, trade references, and surveys. D&B data is used as a general indicator of the local economy and includes information from only those entities that voluntarily report. U.S. Census data from 2020 and FFIEC information from 2025 were used as a standard of comparison for home mortgage lending.

The bank’s record of originating small business and small farm loans contributed more weight to overall conclusions due to the larger loan volumes when compared to home mortgage lending throughout the review period. In addition, while both number and dollar volume of loans are presented, examiners emphasized performance by number of loans because the number of loans is a better indicator of the geographies, businesses, farms, and individuals served.

Conclusions on Performance Criteria

LENDING TEST

Farmers State Bank of Underwood demonstrated satisfactory performance under the Lending Test. The bank’s performance under the Loan-to-Deposit Ratio, Assessment Area Concentration, Geographic Distribution, and Borrower Profile criteria support this conclusion.

Loan-to-Deposit Ratio

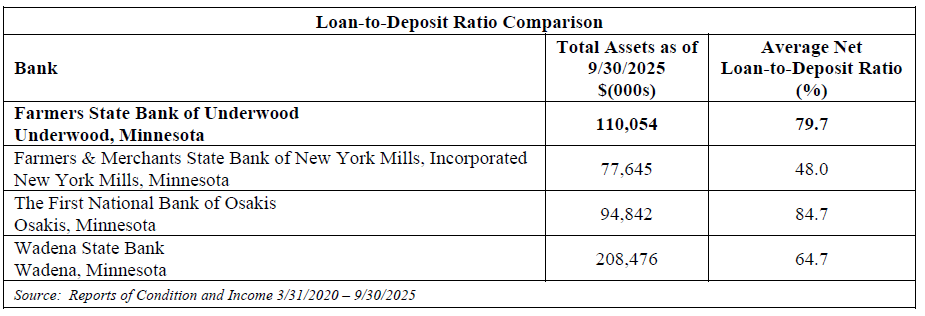

Farmers State Bank of Underwood’s loan-to-deposit ratio is reasonable given the institution’s size, financial condition, and the credit needs of the assessment area. The net loan-to-deposit ratio, calculated from Reports of Condition and Income data, is shown in the following table. The bank’s ratio averaged 79.7 percent over the past 23 calendar quarters and is comparable to the ratios of similarly situated institutions. Similarly situated institutions were chosen based on geographic location, asset size, lending focus, and branching structure.

Assessment Area Concentration

Farmers State Bank of Underwood made a substantial majority of its small business, small farm, and home mortgage loans, by both number and dollar volume, within its assessment area. As previously noted, small business and small farm lending received the most weight in the analysis. See the following table for details.

Farmers State Bank of Underwood made a substantial majority of its small business, small farm, and home mortgage loans, by both number and dollar volume, within its assessment area. As previously noted, small business and small farm lending received the most weight in the analysis. See the following table for details.

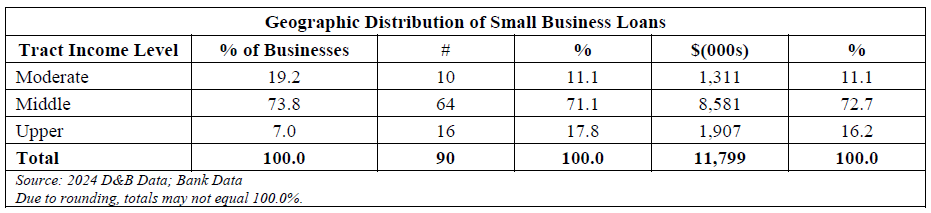

Geographic Distribution

The geographic distribution of loans reflects reasonable dispersion throughout the assessment area. The institution’s reasonable performance of small business, small farm, and home mortgage lending supports this conclusion. Examiners focused on the percentage of loans by number in the sole moderate-income census tract within the assessment area, which encompasses a portion of the City of Fergus Falls.

Small Business Loans

The geographic distribution of small business loans reflects reasonable dispersion throughout the assessment area. As indicated in the following table, the bank’s performance in the moderate-income census tract is lower than D&B data. As previously mentioned, there is a significant level of competition for small business loans in the assessment area. Specifically, there are 11 additional financial institutions directly within the City of Fergus Falls that offer products similar to Farmers State Bank of Underwood. Management confirmed that the subject bank is not a major player in the Fergus Falls market due to the level of competition present. Given this additional information, the bank’s performance is reasonable.

The geographic distribution of small business loans reflects reasonable dispersion throughout the assessment area. As indicated in the following table, the bank’s performance in the moderate-income census tract is lower than D&B data. As previously mentioned, there is a significant level of competition for small business loans in the assessment area. Specifically, there are 11 additional financial institutions directly within the City of Fergus Falls that offer products similar to Farmers State Bank of Underwood. Management confirmed that the subject bank is not a major player in the Fergus Falls market due to the level of competition present. Given this additional information, the bank’s performance is reasonable.

Small Farm Loans

The geographic distribution of small farm loans reflects reasonable dispersion throughout the assessment area. While none of the 72 small farm loans made in the assessment area were in the sole moderate-income census tract, the bank’s lending performance is comparable to D&B data, which shows that only 0.8 percent of assessment area farms are in this tract.

The geographic distribution of small farm loans reflects reasonable dispersion throughout the assessment area. While none of the 72 small farm loans made in the assessment area were in the sole moderate-income census tract, the bank’s lending performance is comparable to D&B data, which shows that only 0.8 percent of assessment area farms are in this tract.

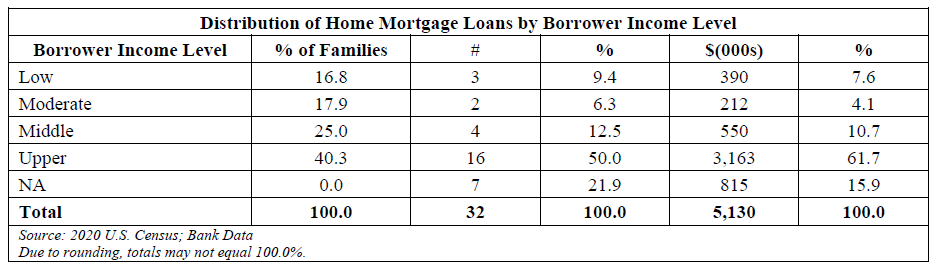

Home Mortgage Loans

The geographic distribution of home mortgage loans reflects reasonable dispersion throughout the assessment area. As shown in the table below, the bank’s performance in the moderate-income tract is comparable to 2020 U.S. Census data.

Borrower Profile

The distribution of borrowers reflects reasonable penetration among businesses and farms of different sizes and individuals of different income levels. The institution’s reasonable small business and home mortgage performance supports this conclusion. Although the bank’s small farm lending performance is excellent, it did not warrant excellent overall performance. Examiners focused on the percentage of loans to businesses and farms with gross annual revenues of $1 million or less and home mortgage loans to low- and moderate-income borrowers.

The distribution of borrowers reflects reasonable penetration among businesses and farms of different sizes and individuals of different income levels. The institution’s reasonable small business and home mortgage performance supports this conclusion. Although the bank’s small farm lending performance is excellent, it did not warrant excellent overall performance. Examiners focused on the percentage of loans to businesses and farms with gross annual revenues of $1 million or less and home mortgage loans to low- and moderate-income borrowers.

Small Business Loans

The distribution of borrowers reflects reasonable penetration to businesses of different revenue sizes. As shown in the table below, the bank’s lending performance to businesses with gross annual revenues of $1 million or less lags the comparable demographic data.

While Farmers State Bank of Underwood is not required to and does not report small business loans under CRA, aggregate CRA data provides context about the size of businesses to which other banks are lending. Aggregate data from 2022 through 2024 revealed that, on average, reporting banks made 58.9 percent of small business loans in the assessment area to businesses with gross annual revenues of $1 million or less. Therefore, the bank’s lending performance is comparable with the average aggregate data. Finally, the 41 sampled loans were made to 31 borrowers. Therefore, when considering the bank’s performance by borrowers, 21 borrowers or 67.7 percent had revenues less than or equal $1 million. Further, as previously mentioned, the bank participated in the SBA’s Paycheck Protection Program, in which the bank originated 263 loans totaling $5,844,624 between 2020 and 2021, demonstrating their willingness to support small businesses. Considering these factors, the bank’s performance is considered reasonable.

Small Farm Loans

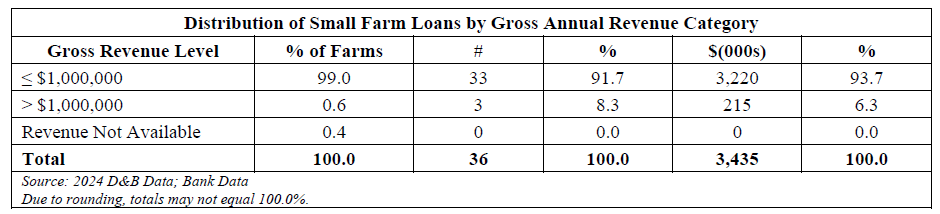

The distribution of borrowers reflects excellent penetration among farms of different sizes. As illustrated in the following table, the bank’s performance is comparable to D&B data but is elevated to excellent when considering 2022 Census of Agriculture data. Per the 2022 Census of Agriculture, 61.3 percent of producers in Douglas, Grant, Otter Tail, and Wilkin counties list their primary occupation as “Other” rather than farming. The 2022 Census of Agriculture also revealed that 65.4 percent of farm operations in these counties did not report interest expenses related to their operations. Bank management confirmed this statement and noted that many farms in the assessment area have off-farm income and do not need credit to finance farm operations. Considering this information, the performance is excellent.

The distribution of borrowers reflects excellent penetration among farms of different sizes. As illustrated in the following table, the bank’s performance is comparable to D&B data but is elevated to excellent when considering 2022 Census of Agriculture data. Per the 2022 Census of Agriculture, 61.3 percent of producers in Douglas, Grant, Otter Tail, and Wilkin counties list their primary occupation as “Other” rather than farming. The 2022 Census of Agriculture also revealed that 65.4 percent of farm operations in these counties did not report interest expenses related to their operations. Bank management confirmed this statement and noted that many farms in the assessment area have off-farm income and do not need credit to finance farm operations. Considering this information, the performance is excellent.

Home Mortgage Loans

The distribution of borrowers reflects reasonable penetration among individuals of different income levels. As illustrated in the following table, the bank’s performance to both low- and moderate-income borrowers is below comparable demographic data. However, the affordability of housing in 2025 inhibited low- and moderate-income borrowers’ opportunities and abilities to qualify for conventional financing. According to 2025 FFIEC data, the maximum income of a low-income family was $47,600 and 2020 U.S. Census cites 5.5 percent of families in the assessment area live below the poverty level. Further, the maximum family income level for a moderate-income family was $76,100 based on 2025 FFIEC data. While the 2020 U.S. Census indicates the assessment area’s median housing value is $195,779; this figure represents the value of all homes instead of home sales or listed for sale. It may be difficult for some low- and moderate-income borrowers to meet standard down payment and underwriting requirements based on housing inventory data from Realtor.com, which cited the 2025 annual average median listing price for Douglas, Grant, Otter Tail, and Wilkin counties was $442,810, $259,048, $396,417, and $330,318, respectively. Additionally, the community contact noted the limited availability of affordable housing. Given these factors, the demand and opportunity for lending to low- and moderate-income families are more limited.

The distribution of borrowers reflects reasonable penetration among individuals of different income levels. As illustrated in the following table, the bank’s performance to both low- and moderate-income borrowers is below comparable demographic data. However, the affordability of housing in 2025 inhibited low- and moderate-income borrowers’ opportunities and abilities to qualify for conventional financing. According to 2025 FFIEC data, the maximum income of a low-income family was $47,600 and 2020 U.S. Census cites 5.5 percent of families in the assessment area live below the poverty level. Further, the maximum family income level for a moderate-income family was $76,100 based on 2025 FFIEC data. While the 2020 U.S. Census indicates the assessment area’s median housing value is $195,779; this figure represents the value of all homes instead of home sales or listed for sale. It may be difficult for some low- and moderate-income borrowers to meet standard down payment and underwriting requirements based on housing inventory data from Realtor.com, which cited the 2025 annual average median listing price for Douglas, Grant, Otter Tail, and Wilkin counties was $442,810, $259,048, $396,417, and $330,318, respectively. Additionally, the community contact noted the limited availability of affordable housing. Given these factors, the demand and opportunity for lending to low- and moderate-income families are more limited.

Finally, 21.9 percent of the home mortgage loans originated in 2025 are commercial purpose/non-owner occupied, such as rental properties, which result in a borrower income level of not available (NA). This skews the lending performance to all income levels. When considering these factors, the bank’s performance is reasonable.

Response to Complaints

The institution has not received any CRA-related complaints since the previous evaluation; therefore, this criterion did not affect the rating.

The institution has not received any CRA-related complaints since the previous evaluation; therefore, this criterion did not affect the rating.

Discriminatory or Other Illegal Credit Practices Review

The bank’s compliance with the laws relating to discrimination and other illegal credit practices was reviewed, including the Fair Housing Act and the Equal Credit Opportunity Act. Examiners did not identify any discriminatory or other illegal credit practices.

Appendices

Small Bank Performance Criteria

Lending Test

The Lending Test evaluates the bank’s record of helping to meet the credit needs of its assessment area(s) by considering the following criteria:

- The bank’s loan-to-deposit ratio, adjusted for seasonal variation, and, as appropriate, other lending-related activities, such as loan originations for sale to the secondary market, community development loans, or qualified investments;

- The percentage of loans, and as appropriate, other lending-related activities located in the bank’s assessment area(s);

- The geographic distribution of the bank’s loans;

- The bank’s record of lending to and, as appropriate, engaging in other lending-related activities for borrowers of different income levels and businesses and farms of different sizes; and

- The bank’s record of taking action, if warranted, in response to written complaints about its performance in helping to meet credit needs in its assessment area(s).

Glossary

Aggregate Lending: The number of loans originated and purchased by all reporting lenders in specified income categories as a percentage of the aggregate number of loans originated and purchased by all reporting lenders in the metropolitan area/assessment area.

American Community Survey (ACS): A nationwide United States Census survey that produces demographic, social, housing, and economic estimates in the form of five-year estimates based on population thresholds.

Area Median Income: The median family income for the MSA, if a person or geography is located in an MSA; or the statewide nonmetropolitan median family income, if a person or geography is located outside an MSA.

Assessment Area: A geographic area delineated by the bank under the requirements of the Community Reinvestment Act.

Census Tract: A small, relatively permanent statistical subdivision of a county or equivalent entity. The primary purpose of census tracts is to provide a stable set of geographic units for the presentation of statistical data. Census tracts generally have a population size between 1,200 and 8,000 people, with an optimum size of 4,000 people. Census tract boundaries generally follow visible and identifiable features, but they may follow nonvisible legal boundaries in some instances. State and county boundaries always are census tract boundaries.

Combined Statistical Area (CSA): A combination of several adjacent metropolitan statistical areas or micropolitan statistical areas or a mix of the two, which are linked by economic ties.

Consumer Loan(s): A loan(s) to one or more individuals for household, family, or other personal expenditures. A consumer loan does not include a home mortgage, small business, or small farm loan. This definition includes the following categories: motor vehicle loans, credit card loans, home equity loans, other secured consumer loans, and other unsecured consumer loans.

Core Based Statistical Area (CBSA): The county or counties or equivalent entities associated with at least one core (urbanized area or urban cluster) of at least 10,000 population, plus adjacent counties having a high degree of social and economic integration with the core as measured through commuting ties with the counties associated with the core. Metropolitan and Micropolitan Statistical Areas are the two categories of CBSAs.

Family: Includes a householder and one or more other persons living in the same household who are related to the householder by birth, marriage, or adoption. The number of family households always equals the number of families; however, a family household may also include non-relatives living with the family. Families are classified by type as either a married-couple family or other family. Other family is further classified into “male householder” (a family with a male householder and no wife present) or “female householder” (a family with a female householder and no husband present).

FFIEC-Estimated Income Data: The Federal Financial Institutions Examination Council (FFIEC) issues annual estimates which update median family income from the metropolitan and nonmetropolitan areas. The FFIEC uses American Community Survey data and factors in information from other sources to arrive at an annual estimate that more closely reflects current economic conditions.

Full-Scope Review: A full-scope review is accomplished when examiners complete all applicable interagency examination procedures for an assessment area. Performance under applicable tests is analyzed considering performance context, quantitative factors (e.g., geographic distribution, borrower profile, and total number and dollar amount of investments), and qualitative factors (e.g., innovativeness, complexity, and responsiveness).

Geography: A census tract delineated by the United States Bureau of the Census in the most recent decennial census.

Home Mortgage Disclosure Act (HMDA): The statute that requires certain mortgage lenders that do business or have banking offices in a metropolitan statistical area to file annual summary reports of their mortgage lending activity. The reports include such data as the race, gender, and the income of applicants; the amount of loan requested; and the disposition of the application (approved, denied, and withdrawn).

Home Mortgage Loans: Includes closed-end mortgage loans or open-end line of credits as defined in the HMDA regulation that are not an excluded transaction per the HMDA regulation.

Housing Unit: Includes a house, an apartment, a mobile home, a group of rooms, or a single room that is occupied as separate living quarters.

Limited-Scope Review: A limited scope review is accomplished when examiners do not complete all applicable interagency examination procedures for an assessment area. Performance under applicable tests is often analyzed using only quantitative factors (e.g., geographic distribution, borrower profile, total number and dollar amount of investments, and branch distribution).

Low-Income: Individual income that is less than 50 percent of the area median income, or a median family income that is less than 50 percent in the case of a geography.

Market Share: The number of loans originated and purchased by the institution as a percentage of the aggregate number of loans originated and purchased by all reporting lenders in the metropolitan area/assessment area.

Median Income: The median income divides the income distribution into two equal parts, one having incomes above the median and other having incomes below the median.

Metropolitan Division (MD): A county or group of counties within a CBSA that contain(s) an urbanized area with a population of at least 2.5 million. A MD is one or more main/secondary counties representing an employment center or centers, plus adjacent counties associated with the main/secondary county or counties through commuting ties.

Metropolitan Statistical Area (MSA): A CBSA associated with at least one urbanized area having a population of at least 50,000. The MSA comprises the central county or counties or equivalent entities containing the core, plus adjacent outlying counties having a high degree of social and economic integration with the central county or counties as measured through commuting.

Middle-Income: Individual income that is at least 80 percent and less than 120 percent of the area median income, or a median family income that is at least 80 and less than 120 percent in the case of a geography.

Moderate-Income: Individual income that is at least 50 percent and less than 80 percent of the area median income, or a median family income that is at least 50 and less than 80 percent in the case of a geography.

Multifamily: Refers to a residential structure that contains five or more units.

Nonmetropolitan Area (also known as non-MSA): All areas outside of metropolitan areas. The definition of nonmetropolitan area is not consistent with the definition of rural areas. Urban and rural classifications cut across the other hierarchies. For example, there is generally urban and rural territory within metropolitan and nonmetropolitan areas.

Owner-Occupied Units: Includes units occupied by the owner or co-owner, even if the unit has not been fully paid for or is mortgaged.

Rated Area: A rated area is a state or multistate metropolitan area. For an institution with domestic branches in only one state, the institution’s CRA rating would be the state rating. If an institution maintains domestic branches in more than one state, the institution will receive a rating for each state in which those branches are located. If an institution maintains domestic branches in two or more states within a multistate metropolitan area, the institution will receive a rating for the multistate metropolitan area.

Rural Area: Territories, populations, and housing units that are not classified as urban.

Small Business Loan: A loan included in “loans to small businesses” as defined in the Consolidated Report of Condition and Income (Call Report). These loans have original amounts of $1 million or less and are either secured by nonfarm nonresidential properties or are classified as commercial and industrial loans.

Small Farm Loan: A loan included in “loans to small farms” as defined in the instructions for preparation of the Consolidated Report of Condition and Income (Call Report). These loans have original amounts of $500,000 or less and are either secured by farmland, including farm residential and other improvements, or are classified as loans to finance agricultural production and other loans to farmers.

Upper-Income: Individual income that is 120 percent or more of the area median income, or a median family income that is 120 percent or more in the case of a geography.

Urban Area: All territories, populations, and housing units in urbanized areas and in places of 2,500 or more persons outside urbanized areas. More specifically, “urban” consists of territory, persons, and housing units in places of 2,500 or more persons incorporated as cities, villages, boroughs (except in Alaska and New York), and towns (except in the New England states, New York, and Wisconsin).

“Urban” excludes the rural portions of “extended cities;” census designated places of 2,500 or more persons; and other territory, incorporated or unincorporated, including in urbanized areas.

Assessment Area Map

Branch Locations

Underwood Branch

110 Main St.

Underwood, MN 56586

110 Main St.

Underwood, MN 56586

Lobby Hours

Monday - Friday: 9:00am - 3:00 pm

Monday - Friday: 9:00am - 3:00 pm

Walk Up

Monday - Friday: 8:00 am - 9:00 am & 3:00 pm - 5:00 pm

Drive Up

Monday - Friday: 8:00 am - 5:00 pm

Monday - Friday: 8:00 am - 5:00 pm

Dalton Branch

105 Main St

Dalton, MN 56324

Lobby Hours

Monday - Friday: 8:00am - 5:00 pm

Walk Up

Monday - Friday: N/A

Drive Up

Monday - Friday: N/A

Rothsay Branch

451 Center St

Rothsay, MN 56579

Lobby Hours

Monday - Friday: 9:00am - 3:00 pm

Walk Up

Monday - Friday: 8:00 am - 9:00 am & 3:00 pm - 5:00 pm

Drive Up

Monday - Friday: 8:00 am - 5:00 pm

Fergus Falls

1114 N Union Ave

1114 N Union Ave

Fergus Falls, MN 56537

Lobby Hours

Monday - Friday: 9:00am - 3:00 pm

Walk Up

Monday - Friday: 8:00 am - 9:00 am & 3:00 pm - 5:00 pm

Drive Up

Monday - Friday: 8:00 am - 5:00 pm

Monday - Friday: 8:00 am - 5:00 pm

List of Services Provided

- Regular Checking

- Rewards Accounts

- Regular Savings Accounts

- Money Market Deposit Accounts

- Certificate of Deposit

- NOW and Super NOW Accounts

- IRA

- Health Savings Accounts

- Safe Deposit Boxes

- ID Theft Monitoring

- Business Interest Checking

- Mobile Banking

- Internet Banking

- Electronic Bill Payment

- Electronic Documents

- Agricultural Real Estate Loans

- Agricultural Operations Loans

- Commercial Loans

- Commercial Real Estate Loans

- Home Purchase Loans

- Home Improvement Loans

- Home Equity Lines of Credit

- Small Business Loans

- Constructions Loans

- Consumer Installment Loans

- Overdraft Protection Lines of Credit

- Remote Deposit Capture

- Remote Deposit

- Debit Cards

Fee Schedule

IMPORTANT ACCOUNT INFORMATION FOR OUR CUSTOMERS

from

FARMERS STATE BANK

COMMON FEATURES

Limits and fees - The following fees may be assessed against your account and the following transaction limitations, if any, apply to your account:

Account Research First hour $25.00, each

Additional hour $20.00

ACH Origination fee for one time ACH and set-up of reoccurring ACH $5.00 each

Account Balancing $25.00 per hour

Bill Pay - Monthly (will only be charged after each month of inactivity) $5.00/mo

Electronic Rush Payment $4.95

2nd Day Delivery $14.95

Overnight Delivery $19.95

Cashier’s Check $5.00

Checking inactivity Charge – Monthly $5.00/mo

All non-minor accounts with no activity within the last 6 months, and a balance of less than $50.00, will incur a monthly

inactivity charge of $5.00 per month.

Copy of bank statement $5.00

Debit Card Replacement Card Fee $15

You may not exceed $500.00 in Point of Sale transactions per day.

You may not exceed $500.00 in cash withdrawals per day.

Deposit Return Item charge $10.00

Fax Outgoing, per page $1.00

ID Theft Protection – Monthly $2.00/mo

Credit Monitoring $4.00/mo

Notary Fee $1.00

Overdraft Charge $25.00 each item/daily

limit $125.00

The overdraft charge applies to overdrafts created by check, in-person withdrawal, ATM withdrawal, or other electronic

means as applicable.

Photocopies $0.25

Printed Bank Statements : Ages 18-59 $3.00/month

Ready Reserve Annual Fee $25.00

Remote Deposit Limits

10 Checks per day totaling $5,000.00

OR 20 Checks per month totaling $5,000

Return Item Charge $25.00 each time item

presented/daily limit

$125.00

Safety Deposit Boxes – Rothsay

Small (2.75 X 5) $15.00

Medium (2.75 X 10) $20.00

Large (5.25 X 10) $30.00

Safety Deposit Boxes – Underwood

Small (3 X 10) $20.00

Medium (5 X 10) $30.00

Large (10 X 10) $45.00

Savings Inactivity Charge – Monthly $5.00/mo

All non-minor accounts with no activity within the last 6 months, and a balance of less than $50.00, will incur a monthly

inactivity charge of $5.00 per month.

Service Fee for Online Charitable Donations $1.99

Stop Payments $15.00

Teller Services $1.00

for transactions or inquiries available through internet/mobile banking systems

Wire Transfers

Outgoing $15.00

Incoming $15.00

International $25.00

Loan-to-Deposit Ratio

2026

Quarter 1 - 78.42%

Quarter 2 - 81.47%

2025

Quarter 1 - 79.70%

Quarter 2 - 78.89%

Quarter 3 - 79.25%

Quarter 4 - 85.68%

2024

Quarter 3 - 79.86%

Quarter 4 - 80.03%